Fact-based decision making.

The sales department really wants to land that one project and get it done fast, but is there room for it in the schedule? Despite regular demands made on management to hire more staff, convincing them can be more difficult than expected. After all, we always manage to get things done – just about – with current staffing levels, don’t we? In this blog we discuss how you can use the capacity utilization rate to have evidence-based discussions with, say, management and the sales department.

The capacity utilization rate provides insight into trends in available workable hours with respect to hours consumed (past) and hours required (future). You can view the capacity utilization rate for each individual employee, as well as for job groups and departments. First, we’ll discuss why you should calculate the capacity utilization rate, and then we’ll show you how to calculate it.

Why calculate the capacity utilization rate?

Why should you calculate the capacity utilization rate? We can give you two reasons.

1. You can look into the future

Calculating the capacity utilization rate based on the schedule provides insight into the future workload. It can help you determine whether or not a given project can fit into the schedule. You allocate your available resources (employees and equipment) for upcoming periods on the basis of your current projects. If you then calculate the capacity utilization rate, you can easily see who is available – and when – for new project applications.

If all your resources are fully booked but you don’t want to turn down a sale, you can hire temporary staff or equipment. When all your employees and resources are fully booked for a longer period of time, but the projects keep coming in, you can opt to hire more permanent staff. Based on the capacity utilization rate, you can make a well-reasoned decision to scale up your company based on hard figures.

And it can work in the other direction too, of course. For example, imagine a drop in the number of incoming projects, which means you have excess capacity for the following year. The capacity utilization rate will clearly indicate this and you can then decide to reduce staffing for certain departments or job groups. By gaining this kind of insight in good time you can cut costs and possibly even save your company from financial disaster.

2. You can interpret the past

If you’re looking back at the past, you should ideally use the actual hours worked by employees. This provides excellent insight into productivity and can be used, for example, for employee performance reviews. Service providers often look at the extent to which employees were eligible and thus contributed to the company’s turnover.

By comparing the capacity utilization rates of employees, job groups and departments in the schedule, you also gain a good understanding of who is performing well structurally and who might be too busy because they are often ‘overbooked’. This could indicate a staff shortage or a disproportionate distribution of work within a team. This kind of insight gives managers a good opportunity to make relevant adjustments.

If your company carries out many seasonal projects, a historical analysis of the capacity utilization rate also provides valuable insights into the times of the year when there are peaks and troughs. You can use this as a basis to determine the minimum number of permanent employees you need as well as what kind of additional ‘buffer’ of flexible staff you need. This is how you create a flexible and efficient organisation.

How do you calculate the capacity utilization rate?

Calculating the capacity utilization rate is easy. The formula looks like this:

The capacity utilization rate is usually expressed as a percentage, but that’s not always the most useful format. Some departments, such as the sales department, prefer to see how many hours are still available. For example, an account manager can see at a glance whether a 100-hour project can still be carried out by an employee or department. For the account manager, 150 available hours means more than 77% capacity utilization.

We need two ingredients to calculate capacity utilization: workable hours and booked hours. In addition to these two ingredients you need to determine for whom you will calculate the capacity utilization rate. You can do this for individual employees, for each job group or for each department within your organisation.

Ingredient 1: workable hours

The first ingredient is ‘workable hours’. This is the divisor in the formula. Workable hours means all hours that an employee has available during his contract period. We can illustrate this by means of a sample calculation.

In order to determine the number of workable hours, you need at least a start date for the employee’s contract. In our example we will assume a six-month temporary contract.

Start date: 1 January 2019

End date: 30 June 2019

An end date is not strictly necessary, but if you already know when you are going to dismiss a temporary employee, then an end date is necessary. In this example, if you do not use an end date you will overestimate your capacity. In that case, in your schedule, after the end date of the contract you can then assume that there are no more workable hours.

Our employee has a contract for 40 hours per week. There are 26 weeks in half a year. The calculation is as follows:

![]()

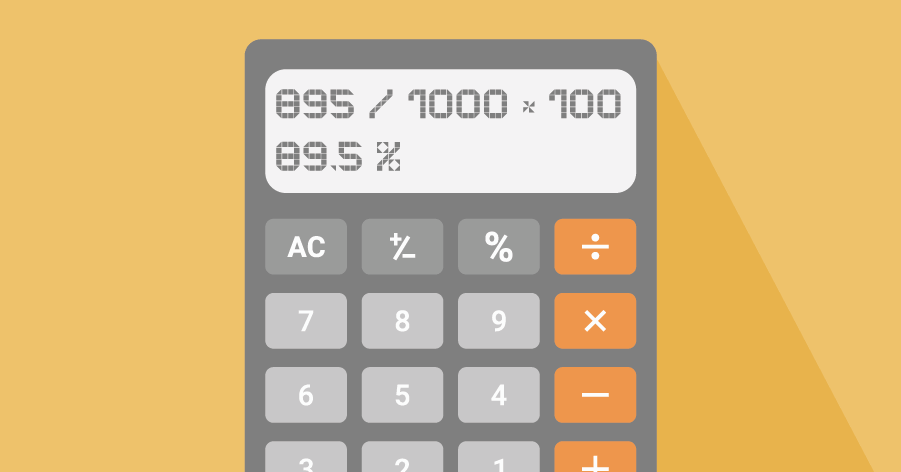

To correctly calculate the workable hours, we need something else. The employee does not work on public holidays, so we have to deduct them from the workable hours. There are five public holidays during the period in question. So we calculate the workable hours as follows:

![]()

This tells us that you can deploy the employee on projects for a 1000 hours. Now you can discuss whether you should also deduct holiday entitlements and the average number of sick days from the workable hours, but we do not think so. You can’t be certain that someone will fall ill or go on holiday during that period. If that happens, the denominator of the formula it is expressed in the booked hours in the denominator of the formula.

Ingredient 2: booked hours

The other ingredient we need in order to calculate the capacity utilization rate is the number of booked hours. This is the denominator in the formula. For the past you can use the actual hours expended by employees. This gives the most reliable picture. If you don’t have this information, you can use scheduled hours from the past. For the future we can only use scheduled hours. This also indicates the importance of good discipline in scheduling. Calculating the future capacity utilization rate depends on this.

The question you have to ask yourself is what type of booked hours you are going to include in the calculation. Will you include all the hours booked in the schedule, including illness, holidays, training and other activities? Or will you include only hours booked on projects? This determines what the capacity utilization rate actually tells you.

If you include all the booked hours, you will get a good idea of the organisation’s productivity. In principle, everyone should reach 100%. If you do not reach 100%, not all employee hours are taken into account. Unused capacity costs a lot of extra money because you have to pay wage costs and there is no value in return.

Many employees will ascribe unused hours to an internal code such as ‘General’ or ‘Other’ so that they will still be at 100%. So it is useful to be able to base the capacity utilization rate on billable or chargeable hours. This filters out general activities such as holidays, illness, training, etc. and creates a picture of productivity in the light of the projects that make money for our company.

Billable or chargeable

It is often useful to distinguish between billable hours and chargeable hours. Billable hours are the hours for which an invoice is actually sent to a customer. It is not useful to only review employees’ performance based on billable projects. Employees often also work on internal projects that are of strategic importance. By classifying both billable projects and internal projects as chargeable, the chargeable percentage provides a better basis for assessing employees.

Conclusion

Calculating the capacity utilization rate is not difficult. You need two ingredients: workable hours and booked hours. If you use software for scheduling and recording actual hours worked, you already have this information at your disposal.

The capacity utilization rate enables you to make well-reasoned decisions about your workforce. You can use the capacity utilization rate to monitor the performance of individual employees, job groups and entire departments. In addition, the sales department can see at any time whether or not a project fits into the schedule. This optimises communication between departments.

We recommend using a professional tool to ensure the capacity utilization rate is always up to date. You can of course calculate it monthly in a spreadsheet, but changes in scheduling, staffing and the project portfolio are a daily occurrence in many organisations. In those cases, a monthly snapshot is simply not good enough because it gives you only 12 times each year to discuss and make adjustments to your organisation. Ideally, you should be able to do this whenever you want based on the most recent information.